The CIO’s Take:

Since late October, long bonds have experienced a sharp reversal, rallying in price as yields plummeted. In recent weeks, that dynamic has seen the term spread go negative: a place it’s often been since 2021, and usually a sign of impending recession. We see this as a bearish development. Despite the bright side of softening economic data—namely, the positive effect weaker growth should have on disinflation—not only do we believe supply and demand in the Treasury market will continue to pressure rates higher, we also see falling yields over the past few weeks as a sign smart-money bond investors are betting on something breaking in the US economy, such that the Fed is forced to cut rates in 2024. We view that as a real possibility and remain firmly in “risk off” mode, underweight equities and overweight low-duration Treasuries. Of course, the threat of a downturn extends to stocks in the popular AI theme. While industry leader Nvidia’s shares certainly aren’t cheap, there’s enough of a fundamental growth story there to warrant further upside—especially if geopolitics turns out not to be as devastating to the firm’s business as some investors imagine.

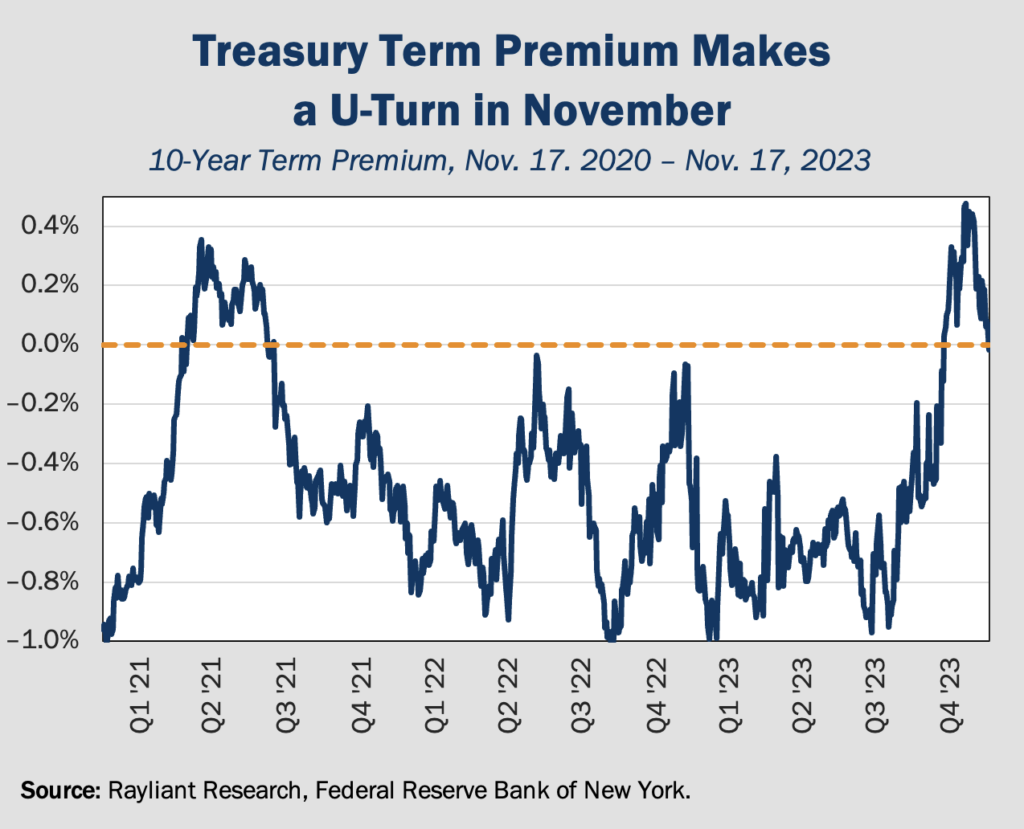

Negative term premium a recession signal

In the last few weeks, we’ve commented on the surge in longer-term Treasury yields, inflicting pain on bond investors and piling on borrowing costs for everyone from the US Treasury itself to companies rolling over their debt and American consumers, whose ability to borrow has been one of the key factors allowing the US economy to grow as fast as it has, despite many pundits and economic indicators predicting recession over the last two years. Indeed, one of the alarm bells ringing for some time was an inverted yield curve: the commonly cited condition in which long-term rates—which are typically higher to give investors locking their money up for an extended period a bit of a “term premium”—actually go lower than short-term rates. When short-term yields exceed long-term yields, the classic interpretation is that the bond market is predicting a recession that will force the Fed to cut currently high rates at some point in the longer-term.

Bond rally puts pressure on long-term yields

That’s what bonds were telling us over the last two years, up until August, when climbing long-term yields pushed the term premium higher, tipping it back into the black in late-September (see below). Interestingly, however, the last few weeks have seen this trend sharply reverse, with the term premium plunging back into negative territory since late October. That “U-turn” in rate differentials reflects a strong retracement in longer-term Treasury yields. Part of the story has been a sudden shift in sentiment to “risk-on,” with Wall Street bulls piling into an “everything rally” trade, emboldened by a range of softer-than-expected economic data—including solid disinflation in recent months—which has prompted expectations the Fed will call it quits on rate hikes and even start cutting by middle of next year. Predictions of a more dovish Fed would certainly explain why investors have suddenly priced in lower longer-term rates. Improved sentiment also jibes with a rally in true risk assets: US stocks and high-yield bonds.

Hedge funds unwinding bets against bonds

Unfortunately, we believe there’s more to the story, and not all of it good news for investors in bonds and risk assets. For one thing, many analysts looking at the last few weeks’ striking decline in yields—10-year Treasuries have dropped more than half a percentage point from a 16-year high in October—note that such a rapid drop must be at least partly driven by a more technical feature: what’s known as “short covering,” whereby sophisticated investors like hedge funds and prop traders close out profitable bets against long-term bonds, requiring them to buy bonds they had previously sold, driving up prices and sending yields lower.

But don’t bet on bond yields continuing to fall

In fact, short covering is a rather benign explanation for a falling term premium. Our bigger concern relates to one of the reasons smart-money investors have cited for taking money off the table: what they see as increased risk of a hard landing, which could lead the Fed to slash rates in 2024, sending bond prices higher. We agree that chances of a soft landing have marginally declined, which is why we aren’t herding with the bulls to load up on risky stocks. On the other hand, as we’ve discussed over the last few months, we see further Treasury issuance and growing concerns over America’s debt and ongoing deficits continuing to pressure long-term yields higher. Together, these two concerns, heightened recession risk and fundamental upward pressure on long-term yields, lead us to continue favoring an allocation to shorter-term Treasuries.

OpenAI’s Altman unexpectedly terminated

Just over a week ago, on Friday, November 17th, the tech world was stunned by an abrupt announcement on a blog at OpenAI—the company best known for its popular AI-based chatbot, ChatGPT—that its influential co-founder and CEO, Sam Altman, was being ousted by the firm’s board of directors. The board gave little explanation for the move, beyond stating that Altman had not been “consistently candid in his communications with the board.” Shortly after Altman was fired, Greg Brockman, another co-founder and chairman of OpenAI’s board, tweeted that he had resigned upon learning the board planned to boot him from the company, as well, attributing the surprise attack to a group of his fellow board members. While gossip is known to quickly spread amongst Silicon Valley insiders, nobody seemed to know why Altman was being purged from the company he started back in 2015.

Clues to board’s rationale in OpenAI’s history

Just about eight years ago, when Altman co-founded OpenAI as a nonprofit, the company’s focus was on prioritizing safety over profits and breaking the grip of foreign governments and entrenched juggernauts like Alphabet, Amazon, and Meta on emerging technologies in the field of artificial intelligence. As research progressed, OpenAI quickly realized the need for capital to make substantial investments in computing resources and top industry talent in its quest for world-changing AI. Altman’s solution was to reform part of OpenAI as a “capped profit” enterprise, balancing the firm’s original altruistic mission with a structure that would meet the capital needs of a company reaching for such ambitious goals. An upshot of that arrangement was that a nonprofit board came to govern a profit-oriented business. Some speculated that Altman’s aggressive agenda for monetizing OpenAI’s breakthroughs had irritated more idealistic members of the board, leading to his ouster.

Microsoft helps put Altman back on the throne

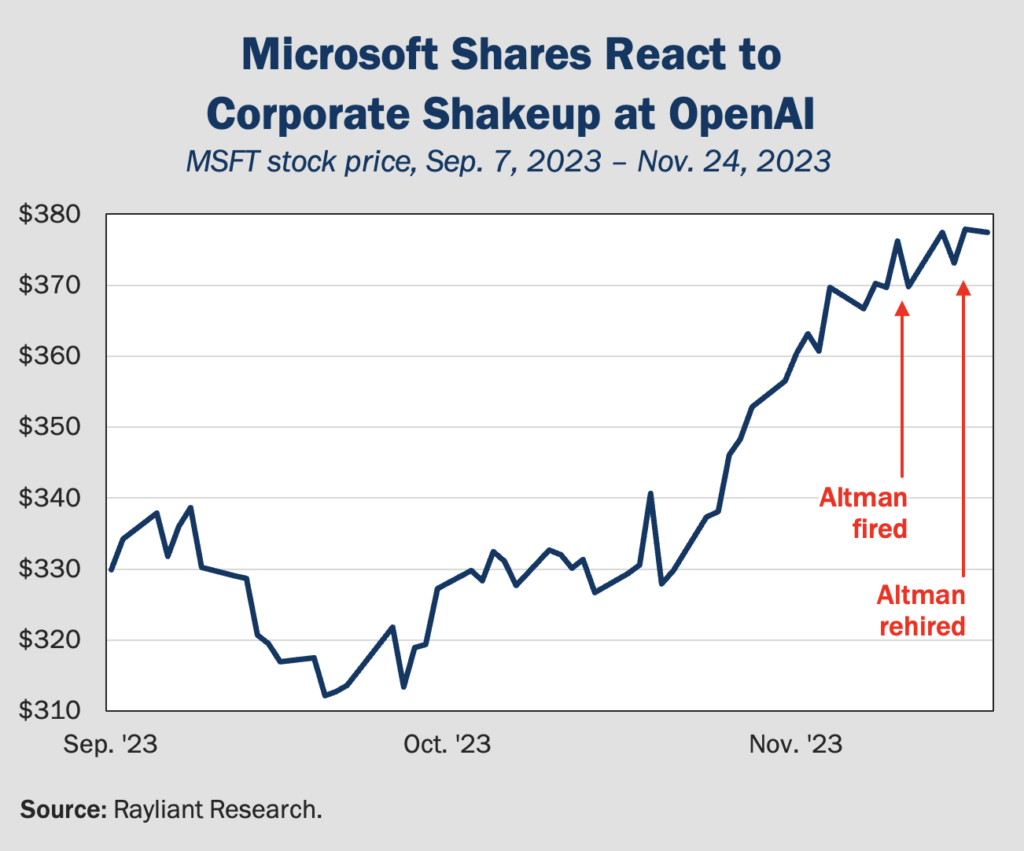

One company with a lot to lose in the face of OpenAI’s leadership shakeup was Microsoft, whose partnership with OpenAI to deploy ChatGPT in its search engine and applications, along with an estimated $13 billion Microsoft has previously invested into OpenAI—without board representation, we might add—were thought to be placed at risk with drama at the firm. Indeed, despite being OpenAI’s most significant backer, executives at Microsoft reportedly only learned of the planned firing minutes before the blog post went public; MSFT shares fell 1.7% in the wake of Altman’s termination, as depicted below).

Of course, the saga couldn’t end there, and Microsoft quickly responded by hiring Altman to lead its own AI research effort, bringing Brockman onboard, as well. That prompted a 2% rally in MSFT stock, as can be seen above. The vast majority of OpenAI employees subsequently signed an open letter threatening to follow Altman over to Microsoft if he wasn’t re-hired. Last Wednesday brought the biggest surprise, as OpenAI reshuffled its board and hired back Altman and Brockman. Microsoft’s stock inched up to a new high.

NVDA reports another mind-blowing quarter

If not for the corporate theatre just described, the spotlight in the AI world would surely have been on Nvidia—the company whose chips power OpenAI’s model—which reported its third-quarter results after the bell last Tuesday. Continuing the firm’s phenomenal growth story, NVDA announced record revenues of $18.1 billion for the quarter, a striking 206% increase year-over-year, and well ahead of consensus estimates for $16.1 billion. Net income likewise soared to $10 billion, marking a 50% increase from the previous quarter and an impressive 580% year-on-year expansion. The firm’s Q3 success was largely attributable to its data center revenue, which hit $14.5 billion for the quarter, up 279% from the previous year, as tech giants like Google, Amazon, and Microsoft move to enhance their AI capabilities.

Understanding the market’s tepid reaction

Prior to reporting, Nvidia’s stock briefly reached a record high of $499.4 before a slight retreat, elevating the firm’s market capitalization above $1.2 trillion. Even so, NVDA shares ended the week down -3.4%. How can that be after such strong results? Glass half empty, it’s easy to put the stock’s post-earnings slump down to valuation: with high expectations priced into the shares, even great results could be prone to disappointment. While we view the shares as expensive, the company’s growth has been nothing short of astonishing, and though the stock trades at a trailing P/E of 61x, based on analyst forecasts, the price is a more reasonable 24x forward earnings. We tend to agree with the bulls that last week’s decline likely reflects management comments around US export controls on Nvidia’s chips—but also align with analysts who point out the firm’s ability to prioritize orders from US firms, making geopolitics a less significant risk in the near-term.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED