The good news is the dollar is likely to stay the world’s reserve currency. The bad news is that the dollar is likely to stay the world’s reserve currency.

In Washington, the status of the dollar as the world’s reserve currency is treated much like the Crown Jewels—something to be guarded jealously, polished regularly, and displayed as proof of imperial virility.

As a Brit, I feel a certain grim duty to warn you: we have seen this play before. It tends to end with a rather nasty hangover.

For the better part of a century, the British Pound held the role the dollar occupies today. We, too, conflated a strong currency with a strong nation. We, too, believed that having the world finance our deficits was a stroke of genius and felt the need to defend it against a fast-emerging industrial power (that’s you Americans, by the way).

But as we discovered in the early twentieth century, when we crucified our industrial base on a cross of gold to keep the Pound strong, being the world’s banker is less of a privilege and more of a burden.

The mechanism is painfully simple, though rarely discussed at fashionable cocktail parties in the Hamptons that I am seldom invited to.

The world runs a savings surplus—mainly from Germany, Japan, and China—and needs somewhere to put it. Because the United States has the deepest, most liquid financial markets, that money flows into New York.

But here is the rub: the Balance of Payments is an identity, not a suggestion or piece of policy. If the world dumps its excess savings on you (a Capital Account surplus), you have no choice but to run a Trade Deficit. The influx of foreign capital bids up the price of the dollar well beyond what trade fundamentals would justify.

Consequently, American manufacturing becomes structurally uncompetitive. It is not that your factories are inefficient; it is that they are being priced out of the market by the very currency they invoice in.

This arrangement creates a rather stark divide in your economy, one that feels increasingly brittle.

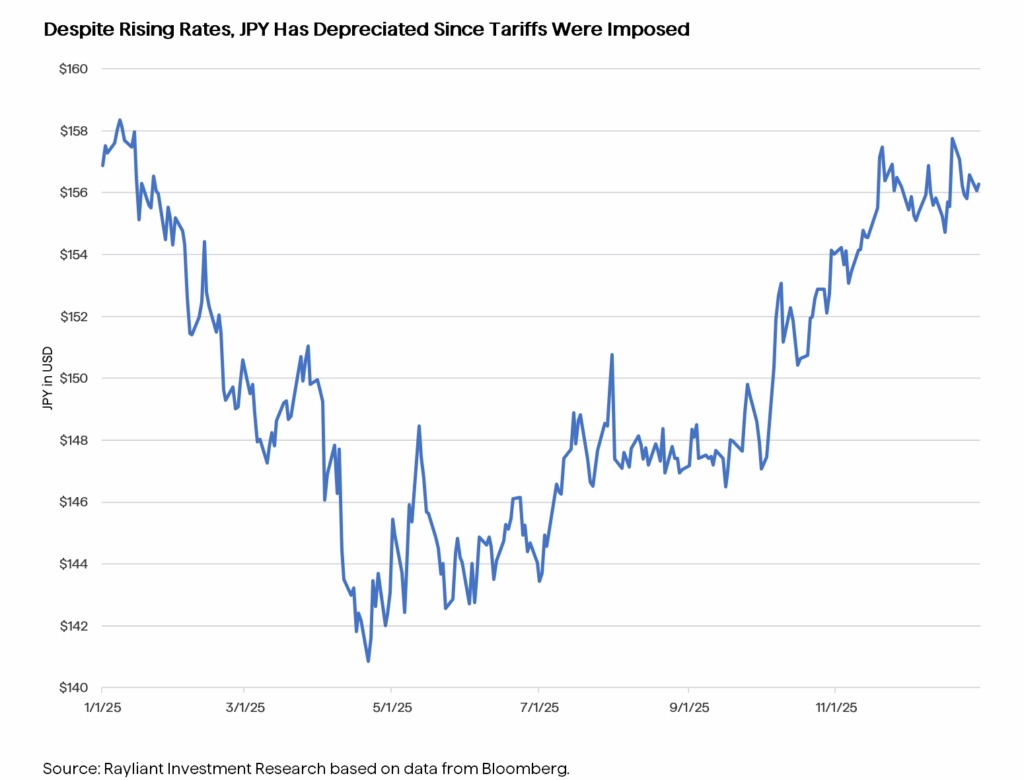

Current policy seems obsessed with tariffs. While politically fashionable, tariffs are a bit like trying to stop a flood with a spoon.

For example, if you slap a tariff on Japanese goods but continue to allow Japanese capital to flow freely into US Treasuries, the dollar will remain overvalued and may appreciate over time.

The price advantage you tried to create for the American worker is erased by the currency market before the ink on the legislation is dry. You cannot fix the trade balance without fixing the capital balance.

The solution is technically straightforward but ideologically heretical to modern investors. To restore competitiveness to Main Street, the United States would need to manage its Capital Account.

This means restricting foreign nations’ ability to dump excess savings into American assets—perhaps through a Market Access Charge or similar tax on inflows. By making it slightly more difficult for the world to buy dollars, you lower its value to a level where American industry can actually compete.

I realise suggesting capital controls to an American audience is akin to serving only vegan cutlets at a barbecue. But the truth is, the current regime is in fact the aberration, not the norm. The Bretton Woods system, which ran from 1944 to 1971, had explicit capital controls. The United States also had the Interest Equalization Tax until 1974 and there was the Plaza Accord in 1985.

The current regime only congealed in the 1990s under the Clinton administration and Robert Rubin. Rubin was, of course, ex-Goldman Sachs and Wall Street, and the likes of Goldman have been some of the biggest beneficiaries. This, combined with equally ill-thought-out measures like NAFTA and the WTO, accelerated America’s industrial decline and led to the “China shock.”

Once we accept that the US dollar’s “privilege” has become an economic straitjacket, the natural question is: when does the straitjacket snap? And more importantly, where should one be standing when it does?

Unfortunately, predicting currency regimes is usually a fool’s errand—the graveyard of macro traders is paved with “Short Dollar” theses—but structural shifts do not come out of nowhere. The British Empire didn’t end on a Tuesday; it was a long, slow erosion followed by a sudden dam break (admittedly accelerated by unwanted M&A from our European competitors). Here is what we are watching, and how we would react.

We are looking for a shift in the plumbing, and actually, they are almost all there:

This is the final sign we need to trigger a regime shift. And at this point, we need to rethink asset allocations—unhedged international exposure, real assets, a rotation away from passive US indices. But the specifics are a discussion for another time.

If Washington does move to manage capital flows, the financial press will inevitably frame it as an admission of defeat, the abandonment of American free-market principles. This is nonsense.

The era of completely unrestricted capital flows is not some ancient American tradition. It is a 30-year experiment, born in the 1990s, that has demonstrably failed to deliver for ordinary Americans. The Bretton Woods architects understood that unfettered capital could be as destabilising as unfettered trade was beneficial. They were not socialists; they had lived through the 1930s.

The dollar will remain the world’s most important currency—there is simply no alternative with the depth and liquidity to replace it. The United States built the middle class that made it great before the Rubin doctrine, and it can do so again after.

The United States is, and remains, an exceptional country inhabited by extraordinary people. A rebalancing of the capital account is an economic adjustment, not an existential crisis.

Wall Street will, of course, fight any change to the status quo. They have done rather well from it. But small elites with deep pockets defending their privileges against a restive democratic majority of Americans is not a winning long-term strategy, as your ancestors ably demonstrated to us British.

Disclosure: This material is for informational purposes only and should not be considered investment advice. An investor should consult with their financial professional before making any investment decisions. The opinions contained herein are subject to change without notice and do not necessarily reflect the opinions of Rayliant Investment Research. Indices cannot be invested in directly and are unmanaged.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED