Perspectives

Phillip Wool, Ph.D.

Scroll down

“Each of them spoke a turgid dialect of English that came to be known as ‘Fedspeak’, a term which seems to connote the use of numerous complicated words to convey little if any meaning.”

—Alan Blinder, Princeton Economics Professor, on the perils of parsing Fed chairs’ words

Like many investors, we found ourselves glued to the screen on Wednesday, December 10, 2025. We weren’t so much wondering what the Fed would do: Even the night before the FOMC announced its decision, futures traders seemed to hold the same view we did, that another notch down in interest rates was all but guaranteed, with CME Group data indicating a market-implied probability of a quarter-point cut at over 88% probability. But we did wonder how the news would sound when Powell delivered it at the post-meeting press conference. In particular, we were looking for policy “tells” in the Fed chair’s tone—not to mention the details of voting, the dot plots, and everything else in this meeting’s quarterly edition of the US central bank’s Summary of Economic Projections.

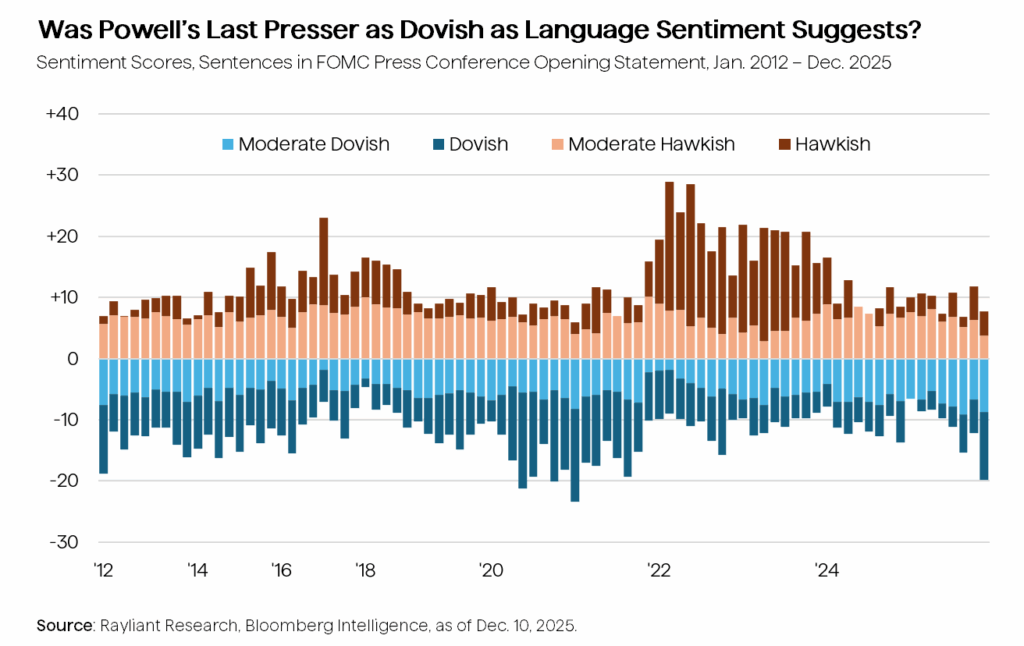

As ‘quantamental’ investors, we’re characteristically interested in the fundamental content of everything surrounding a heavily anticipated Fed meeting, though we also like to see things through a quantitative lens. Judging by natural language processing performed by the folks at Bloomberg Intelligence, plotted below, Chairman Powell’s opening statement to the press after the meeting came in as one of the most dovish since rates began rising back in 2022.

Of course, quant models don’t always capture all of the nuance in something as complicated as human language, and it turns out that some context is probably needed to make sense of the December FOMC transcript. For one thing—as the team at Bloomberg Intelligence aptly noted—the Fed chair made plenty of references to the Fed’s resumption of asset purchases, buying short-term Treasuries, which counted meaningfully toward the model’s sense of dovish sentiment. Powell was careful to note, however, that those bond purchases “have no implications for” the bank’s monetary policy and were really just about managing the Fed’s reserves for the sake of market liquidity.

In our view, bits of Powell’s explanation of the Fed’s deliberations that did sound truly dovish include references to jobs weakness being less about soft labor market growth—in other words, the supply of jobs—and more about sagging demand for hiring. That’s the kind of unemployment risk that would prompt the Fed to keep cutting. He also mentioned that he thinks payroll figures reported previously are likely to have understated the trend down in labor market conditions, once the usual corrections are all in. Likewise, Powell reiterated the consensus that inflation stickiness now is driven mostly by tariffs, which the Committee regards as likely to be a one-off. All of this points to the “balance of risk” still tilting toward employment, suggesting more cuts in store.

On the other hand, a reference in the post-decision statement to the “extent and timing of additional adjustments to the target range” is precisely what the FOMC has said in past instances of pauses in policy moves, contradicting the notion cuts will continue. Likewise, we see Powell’s comment that rates are now “within a range of plausible estimates of neutral” as exactly what one might expect the chair to say in messaging the possibility we’re going to be stuck at this level for at least a meeting or two, until more data come in. Getting closer to neutral—where there might naturally be more disagreement as to where exactly that equilibrium is—would also explain the increase in dissent among Fed officials as to whether December should have been a cut or a hold.

Sentiment notwithstanding, shortly after the Fed’s decision and press conference, market-implied forecasts of rate cuts for 2026 jumped out to an expectation for 50 bps more of easing next year, in stark contrast to the FOMC’s dot plot, which showed just one additional cut slated over the next 12 months. While we can’t argue with the plausibility of more easing than the dots indicate, and natural language sentiment scores seem to point in that direction, one thing we regard as pretty much a sure bet for the new year is continuing policy uncertainty—and plenty more fussing over every little word the Fed chair speaks.

Disclosure: This material is for informational purposes only and should not be considered investment advice. An investor should consult with their financial professional before making any investment decisions. The opinions contained herein are subject to change without notice and do not necessarily reflect the opinions of Rayliant Investment Research. Indices cannot be invested in directly and are unmanaged.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED