The London edition of the Financial Times took a rare break from its usual fare of either promoting the merits of a Brussels-run command economy or finding some innovative way to manipulate statistics to show that its dire predictions about Brexit were—tragically—wrong to actually report some financial news.

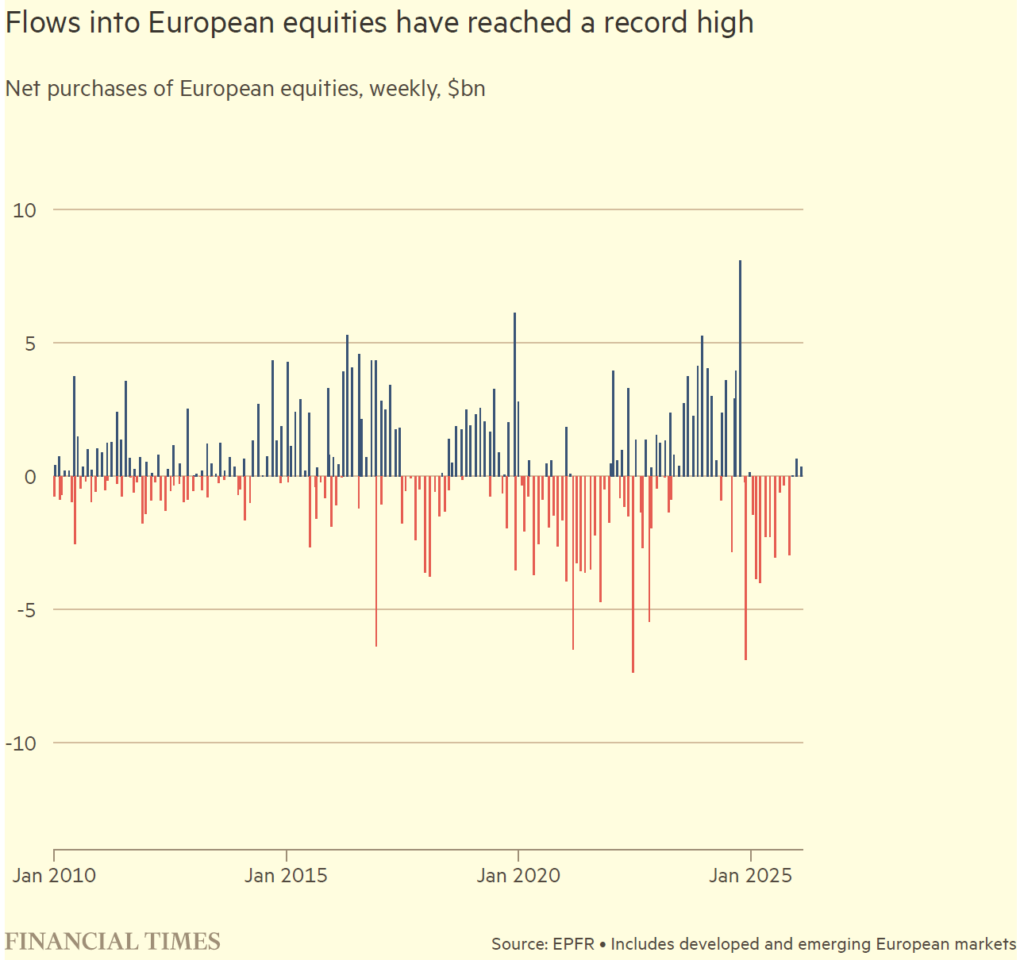

Fortunately for the budding class of nomenklatura that is increasingly making up its readership, it was recently a rare positive for my home continent: European equity markets saw record inflows.

Source: 2026. Herbert, Emily. “Investors Pour Record Sums Into European Stocks,” Financial Times, February 20.

There are good reasons for this. European equities look cheap. On a cyclically adjusted basis, European stocks trade at roughly half the earnings multiple of the S&P 500 Index—the widest valuation gap in a generation. In 2025, the market finally noticed: the STOXX Europe 600 Index returned around 16% for the year, outperforming the S&P 500 in dollar terms for its strongest relative showing in over a decade. European banks alone were up some 65%, their best annual performance since 1997. The rotation was real, and the temptation to rebalance toward Europe is understandable.

But before you pack your bags, it is worth reading the user manual. And understanding why a selective rather than an indiscriminate approach to capital allocation is prudent.

Anyone investing in Europe should understand that what appears to be a valuation opportunity sits atop deeper, slower-moving forces that have been building for decades. The past does not merely influence the present. It constructs it. And Europe’s past is unusually instructive—and alas, predicted.

The historian Tony Judt argued that Europe’s post-war stability was not the dawn of a new epoch but a parenthesis—built on three key factors that were always likely to be temporary: the American security guarantee, a collective determination for unity above all due to the horrors of the war, and economic conditions that were always going to be unsustainable.

Sir James Goldsmith, the financier, arrived at a similar conclusion from a different direction. In the early 1990s, he warned that global free trade would hollow out Europe’s (and America’s) middle classes, that mass migration would follow, and that the social cohesion holding these societies together would fracture under the strain. Both men were largely dismissed at the time. Both now read less like prediction and more like reportage.

This is approximately where we are now. And whilst it might all sound scary, in the grand sweep of European history, none of it is remotely new. It is basically a Tuesday.

That said, forewarned is forearmed—and there are specific dynamics investors should understand.

First, the European Union is failing. It was constructed for a post-war order that no longer exists and lacks the mechanisms and feedback loops necessary to correct itself. And as it fails, it acts as more of a bureaucratic and regulatory drag on the economy.

These words could have come from one of the ever-increasing number of populists, but this is actually the conclusion reached by former ECB President and one of the EU’s High Commissars, Mario Draghi. His report detailing the EU’s growing failures was, in the finest European tradition, ignored. It joined all the previous reports saying the same thing and, probably, joined them in what, in my imagination, looks like the government warehouse at the end of Raiders of the Lost Ark.

The problem is that instead of making a determined attempt to restructure itself, the EU has resorted to an older European tradition: an entrenched, overprivileged class fighting change. This would be recognizable to Machiavelli, who made the same observations about elite self-preservation and institutional decay 500 years ago, drawing on even older Roman sources from nearly 1,500 years earlier, which were themselves based on observations from the centuries before that.

The pattern is always the same: governing classes accumulate advantages, resist reform, and slowly hollow out the institutions they inherited. Growth stagnates. Accountability is treated as an inconvenience. The names change. The dynamics do not. What would constitute a genuine historical surprise is if any of this were not happening.

A good example of this is ECB President Christine Lagarde’s ‘sudden’ retirement. This is to ensure that Macron’s likely populist successor as French president has no say in who Europe’s next top central banker should be. This pattern is being replicated all across France and will likely spread to other states as the old order attempts to build a firewall against the sort of people who rarely read the Financial Times, let alone agree with its mistaken auguries.

The problem is that none of this will be successful. Another European, a certain Karl Marx, observed that ultimately politics will follow economics. If the old order cannot deliver the goods, then expect those pesky populists to keep pushing. This means political instability and the possibility that the usual crackpot ideas—of which Marx himself was no small advocate—will be thrown into the mix.

For investors, the practical question is straightforward: Europe is a system slowly running out of organizational energy. It is not collapsing dramatically. It is failing to renew itself—demographics, productivity, institutional capacity, and political legitimacy all gradually degrading. The trajectory is glacial rather than acute. And glacial trends are the ones that get priced in last.

None of this makes European equities uninvestable. At current multiples, there is a genuine margin of safety in selected names—particularly companies with global revenue streams that happen to be domiciled in Europe rather than dependent on it. Banks benefiting from positive rate dynamics, defense companies riding a structural spending cycle, and industrial exporters with emerging-market exposure all have identifiable near-term catalysts.

But the valuation discount exists for a reason. Europe’s problems are structural, not cyclical. Treat European equity exposure as a tactical allocation driven by valuation, not a strategic conviction driven by fundamentals. Size positions for what Europe is, not what the FT-reading EU apparatchiks hope it might become through a heady combination of long-term economic planning and magical thinking. Capture the re-rating and sector rotation where it presents itself. But do not mistake cheapness for health.

A discounted price is attractive. A discounted civilization rather less so—though Europe has been here before, and the continent has a reliable habit of muddling through, usually at considerable expense to whoever was holding its bonds at the time.

Disclosure: This material is for informational purposes only and should not be considered investment advice. An investor should consult with their financial professional before making any investment decisions. The opinions contained herein are subject to change without notice and do not necessarily reflect the opinions of Rayliant Investment Research. Indices cannot be invested in directly and are unmanaged.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED