“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die in euphoria.”

—Sir John Templeton, legendary mutual fund investor

With nearly a quarter of the year in the books, there seems to be more than enough risk to go around. Of course, we always knew we would have the overhang of tariffs to contend with in 2026, with a number of temporary agreements set to expire and many companies reportedly reaching their limits in terms of how much of the price shock to consumers they’re willing to absorb. Likewise, macro forecasters had previously sounded the alarm over US fiscal discipline and long-term inflation risk, which is complicated this year by the end of Fed chair Powell’s term and mounting concerns over the central bank’s independence. One quarter into the year, we’ve added to that list of worries an energy crisis brewing amidst war in the Middle East, rising fear of AI’s existential threat to American jobs and even entire industries—think “SaaSpocalypse”—not to mention references to “recession” and “stagflation” creeping back into the market chatter.

But how seriously are investors really taking the range of risks staring down markets in 2026?

One way of answering that question is by looking at something called the equity risk premium, a tool economists use when trying to explain how an investor setting his or her asset allocation ought to think about the balance between stocks and bonds in their portfolios. If we consider fixed income and equity securities simply as different ways of delivering cash flows to investors—interest payments on bonds versus earnings and dividends paid to common stockholders—then we might distinguish between these different instruments strictly in terms of the level of risk they bring to an investor’s portfolio. Continuing with that train of thought, it seems reasonable for an investor to wonder how much more “risky” equities will return than comparatively “safe” fixed income. The answer to that question is the equity risk premium.

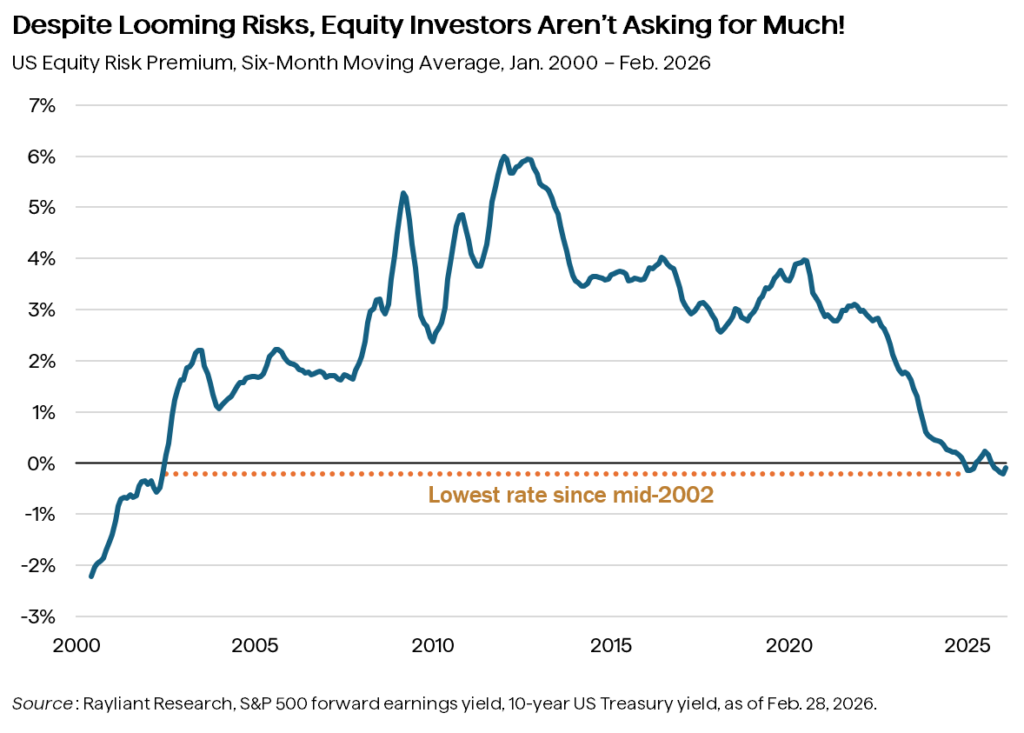

In comparing the risk and reward of stocks and bonds, we need to get things onto an apples-to-apples basis, and there are many ways to do that. Below, I’m plotting one version of that calculation. It’s pretty simple to assume the yield on 10-year US Treasuries represents a relatively low-risk bond return. For the US equity return, we take the forward P/E ratio of the S&P 500 Index and invert it, flipping it into an E/P ratio: the so-called “earnings yield”, which is like the “return” on stocks, if you assume that paying the stock price today entitles you to the company’s earnings at the end of the year—in the same way our annual Treasury yield is just the bond’s payout at the end of a year. Now we simply subtract the lower-risk bond yield from the higher-risk stock yield, and we have the “extra” return stocks are paying for the extra risk a stock investor is taking in the market (i.e., the equity risk premium).

In the graph above, I’ve actually depicted the six-month moving average of the equity risk premium, which I believe helps to iron out some of the noise of month-to-month price volatility and make things a little easier to track. Looking at the chart, we can see that the equity risk premium fluctuates over time, and one interpretation of the ups and downs is that they’re telling us about investors’ changing sentiment toward risk. The premium is rising amidst the dot-com bubble burst, and to me there’s a clear spike around the Global Financial Crisis, and another bump around the COVID crash. There are basically two things going on here: When the situation gets risky, stocks often fall—investors sell until the price implies a forward return attractive enough to buy again—and bonds rise, amidst a flight to safety and, often, central bank stimulus. That helps to explain why the equity risk premium sunk so low post-pandemic, with stocks and rates both rising.

While the equity risk premium is clearly just one lens through which to view the economy and markets, it seems like a good one for the moment we find ourselves in today, with stocks still trading pretty close to all-time highs, even as that litany of risks I mentioned threatens the bull-market narrative. At the far right of the chart, we see that—with the exception of a blip in 2025 as stocks faced a short-lived sell-off in response to “Liberation Day”—the equity risk premium is mostly negative. In other words, not only are investors in stocks not receiving any extra return for risk, they’re actually paying for it. That doesn’t necessarily mean investors should avoid stocks: earnings growth can raise the equity risk premium just as well as falling prices. It does suggest, however, that those “buying the dip” today are taking a much greater leap of faith than in times past when it comes to earning the bonus yield that makes such extra risk worth taking.

Disclosure: This material is for informational purposes only and should not be considered investment advice. An investor should consult with their financial professional before making any investment decisions. The opinions contained herein are subject to change without notice and do not necessarily reflect the opinions of Rayliant Investment Research. Indices cannot be invested in directly and are unmanaged. The equity risk premium (“ERP”) is a a framework and not a forecast and may not fully capture market dynamics. Forward P/E and E/P are hypothetical constructs and do not guarantee returns.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED