Perspectives

Phillip Wool, Ph.D.

Scroll down

“Economists are basically unanimous that Fed independence is critically important.

And to see why, just look at the countries where they don’t have Fed independence.

Inflation is higher, unemployment is higher, growth is worse.”

—Austan Goolsbee, Chicago Fed President, speaking to CNBC in April 2025

Sometimes there’s uncertainty about what the Fed will do at an FOMC meeting. That definitely wasn’t the case when policymakers convened late last month, with Fed funds futures pricing in virtually zero probability of anything but a continuation of the central bank’s hold on US interest rates. Instead, what kept us all glued to the TV during the Fed’s post-meeting presser was a knowledge that it would be Jay Powell’s last Q&A as Fed chair—his term ended on Friday, May 15, 2026—and perhaps a question as to how he would choose to end things: Would he ride off into the proverbial sunset after eight years at the helm, or stick around on the Board of Governors, a role that could keep him at the bank into 2028?

Despite the Fed predictably standing pat on rates, those who opted to tune in for Powell’s swan song enjoyed plenty of drama, as the outgoing chair did end up exercising his right to hang around as a voting member of the Board of Governors—something that hasn’t happened since 1948. During the press conference, Powell argued that “things that have happened, really in the last three months, have left [him] no choice” but to remain on the board and, one presumes, fight to defend the central bank’s independence against challenges from President Trump’s White House.

Chief among those threats, according to critics of the administration, was a criminal probe by the Justice Department into Powell’s handling of Federal Reserve building renovations. That investigation was halted in late April—allowing a Senate Banking Committee vote to confirm the next Fed chair, Kevin Warsh, to go through in the nick of time—though with no exoneration of the Fed chair and a suggestion that the probe might be resumed at any time. Such conditions didn’t lend enough “transparency and finality,” in Powell’s words, to give him sufficient confidence the Fed would continue to operate free from political coercion.

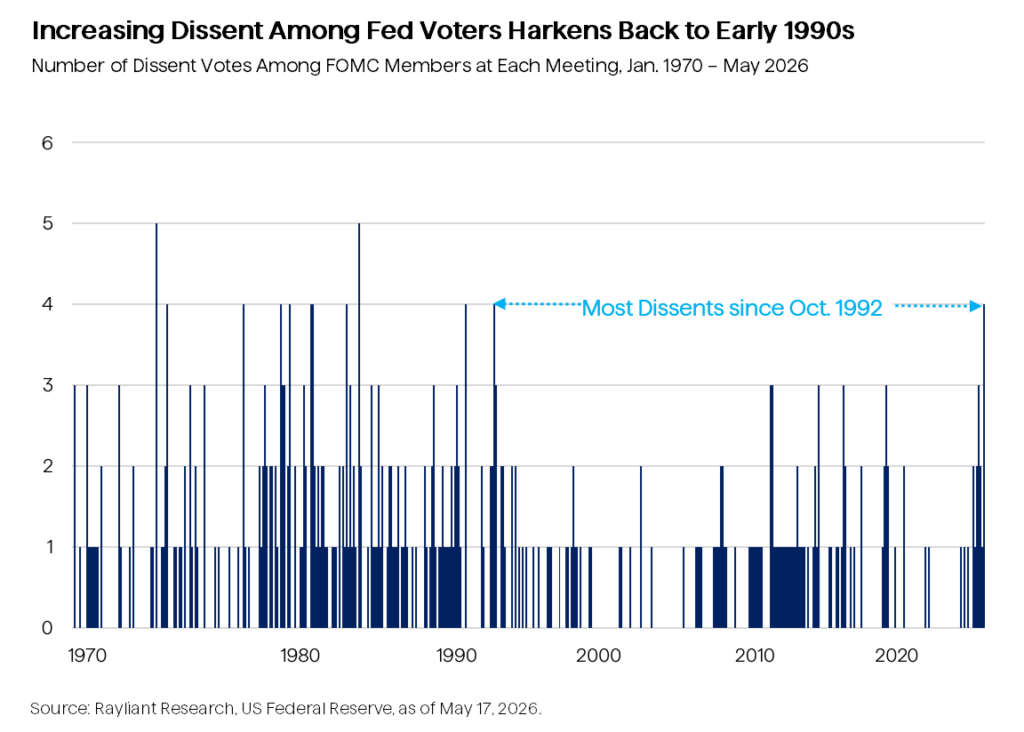

Powell’s choice to postpone his retirement would have been big enough news for pundits to digest, though it wasn’t the only surprise stemming from late April’s meeting. While the policy vote’s outcome was entirely expected, the breakdown of yeas and nays yielded another interesting conclusion: there were an extraordinary four dissents included in the tally, three of which came in against expressing any sort of an easing bias in the FOMC’s post-meeting statement; the fourth was Stephen Miran’s expected preference for a quarter-point cut versus a hold on rates. That may not seem too contentious, but it turns out to be the most dissenting votes against Fed action (see below) since way back in October 1992, when Committee members were debating a continuation of easing amidst a weak economic recovery.

In the context of Powell’s choice to remain a voting member of the board, growing division within the FOMC is particularly salient: It effectively prevents Warsh and Miran from both casting a pro-Trump vote on future rates decisions, most likely forcing the temporarily appointed Miran to resign in order to vacate a seat at the table for the new chair. Although Powell has been adamant that he has no intention of becoming a “shadow chair” at the Fed (“I’m not looking to be a high-profile dissident, or anything like that,” he said during his farewell press conference), it’s hard to imagine the dynamic not being awkward with strong voices of the past and present inevitably influencing two sides of an increasingly tenuous consensus.

On the other hand, as we’ve mentioned before, there’s something very natural and actually quite healthy about debate intensifying as rates narrow down to a probable “neutral” range. That’s especially true amidst the kind of pronounced uncertainty in the data that has accompanied last year’s tariff threats and the massive energy shock from this year’s conflict in the Middle East. Indeed, it seems likely to us this challenging setup for inflation is more to blame for traders’ increased pessimism over further easing, and that—uncomfortable as the “old-and-new-chairs” dynamic might be—Powell will ultimately seek to avoid the limelight and quite possibly find an off-ramp from the Board as soon as the Fed’s inspector general, currently auditing Powell’s building project, absolves him of any wrongdoing.

Until then, just make sure you’ve got the popcorn ready for June’s FOMC, where Kevin Warsh is almost set to make what will, one imagines, be an appropriately dramatic debut!

Disclosure: This material is for informational purposes only and should not be considered investment advice. An investor should consult with their financial professional before making any investment decisions. The opinions contained herein are subject to change without notice and do not necessarily reflect the opinions of Rayliant Investment Research. Indices cannot be invested in directly and are unmanaged.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED