“He had just enough money to last him a lifetime, unless he bought something.”

— Saki

The current enthusiasm for Artificial Intelligence has become the most extravagant single-sector investment boom in American corporate history. With global capital expenditure expected to eclipse $500 billion this year against actual end-customer revenues of perhaps a tenth of that figure, the numbers are frightfully large; the chasm between them is larger still. For equity investors, the question is whether AI will deliver a sufficient return on capital. For fixed-income investors, the question is far simpler: who is funding this staggering outlay, and what breaks when the cash arrives unfashionably late?

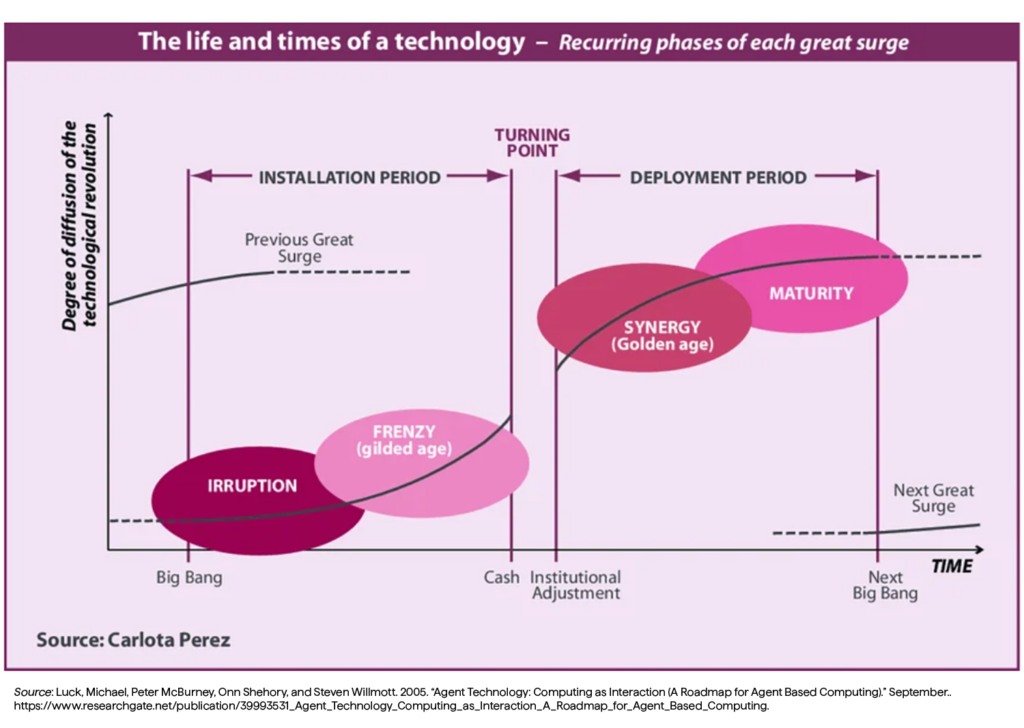

This is not, however, an original sort of folly. Carlota Perez’s rather brilliant framework of technological revolutions instructs us that major technologies move through two great phases, conveniently separated by a financial crisis. In the “installation phase,” capital insists on funding infrastructure ahead of any actual demand, pricing the novelty on the breathless presumption of what it might eventually achieve. Later, in the “deployment phase,” after a crisis has graciously swept away the more excessively enthusiastic participants, the surviving infrastructure is put to productive use. The pattern recurs with the tiresome predictability of the English being prematurely eliminated from the world finals of a sport we ostensibly invented.

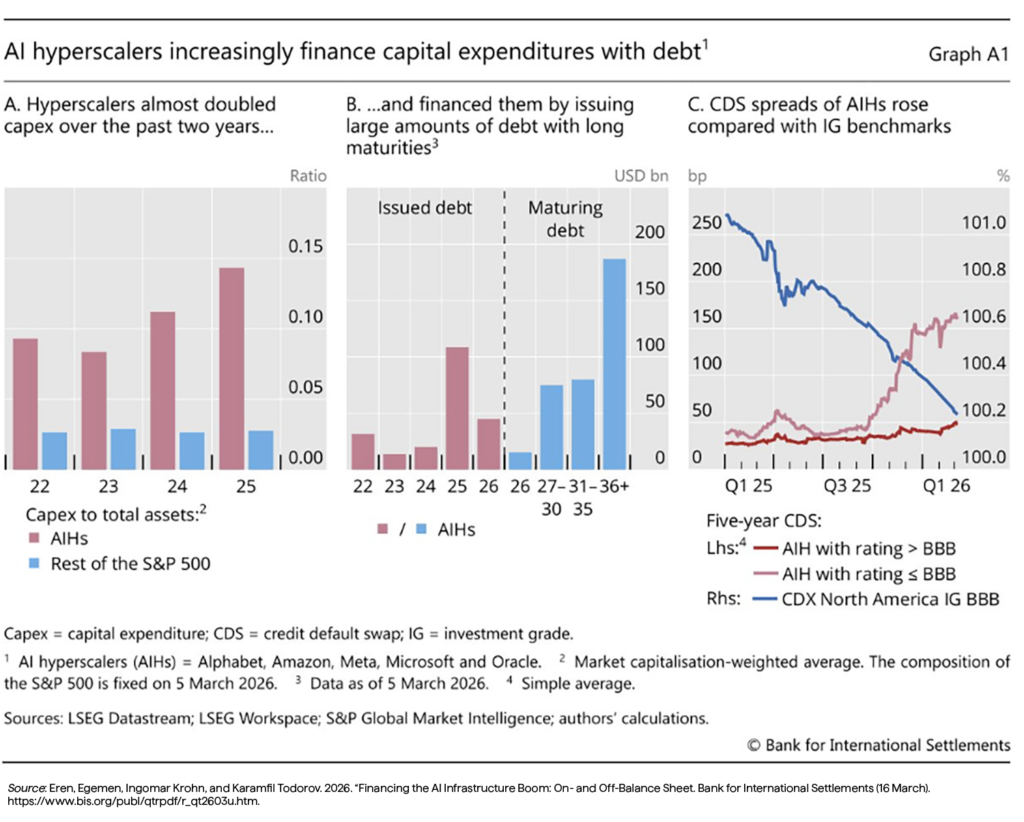

Consider the funding. The operating cash flow of the major hyperscalers is no longer sufficient to cover their ruinously extravagant toys. The gap is being papered over by equity issuance, vendor financing, and a remarkable expansion of private credit—a market now asked to finance long-duration assets with deeply impatient capital. These funds boast quarterly redemption provisions that one imagines will be severely tested during any meaningful market unpleasantness. It would be profoundly unwise to be found holding such ill-bred instruments when the music inevitably stops, and the chairs are abruptly removed. The entire edifice rests upon a rather fatal duration mismatch: five-to-seven-year projects funded by investors whose tolerance for delayed gratification is notoriously short.

And then there is the tricky problem of the physical substrate itself. Unlike a nineteenth-century railway, which had the decency to remain useful even after comprehensively bankrupting its original founders, a GPU simply becomes passé in three to five years—the technological equivalent of last season’s hat. What actually survives the inevitable crisis is merely the boring infrastructure: the cooling systems, the building shells, and the regulatory permits.

Speaking of power, the intelligent observer must also prepare for the inevitable steepening of the yield curve. When the enthusiasm falters and the cycle breaks, central banks will undoubtedly slash short-term rates in a desperate bid to soothe panicked markets. Yet, the long end of the curve will remain stubbornly elevated, anchored by structural inflation and the exorbitant energy costs required to keep these machines humming. This stickiness is, of course, entirely unhelped by the ongoing skirmishes in Iran, which continue to propel energy prices skyward on the wings of yet another “imminent” and highly publicized peace deal that never quite materializes.

The sensible fixed-income investor avoids the undignified scramble of attempting to divine which specific technology applications will prove transformative. Instead of opining on the winners of a technological pageant one scarcely understands, the relevant questions are far more pragmatic:

It is far better to maintain a liquidity position for a risk-off event, capture the energy input-cost asymmetry, and prepare for inevitable issues with the yield curve. The fixed-income investor is not paid to decide which chatbot, algo, or chip wins the pageant. We are paid to judge whether the funding structure can survive a slower path to profitability. In installation phases, that is usually the only question that matters.

This material is for informational and educational purposes only and should not be considered investment advice or a recommendation to buy or sell any security. The author, Ben Ashby, is Chief Investment Officer of Henderson Rowe, an affiliate of Rayliant Investment Research. The opinions expressed are those of the author as of the date of publication, are subject to change without notice, and do not necessarily reflect the opinions of Rayliant Investment Research or its affiliates. Certain statements are forward-looking and reflect the author’s views on future market conditions; actual results may differ materially. Investors should consult their financial professional before making any investment decisions.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED