The events of late February and early March in the Middle East have generated enormous noise. My aim here is to cut through that noise and focus on what matters for investors.

I spent several years running businesses across the MENA region. I have spent a considerable amount of time in the Gulf—meeting counterparts, understanding how the region functions operationally, and watching how it responds under pressure. I say this because what follows is grounded in that experience, and some of it runs counter to what I am currently reading in the mainstream financial press.

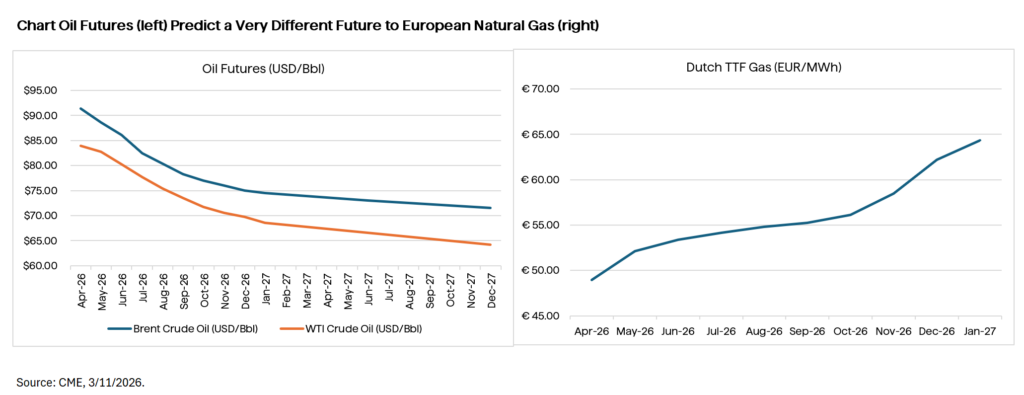

The dominant market narrative is straightforward: a significant military event has occurred, energy prices have spiked, but the situation will stabilize, the Strait of Hormuz will reopen under some form of international arrangement, and within 6 to 12 months we return to something resembling prior equilibrium. Crude futures curves reflect exactly this view—front-end prices have moved sharply, but the back end of the curve, looking out to late 2027, is priced for resolution.

I think that framing misses the structural complexity of what is actually happening. The market is conflating two separate questions. The first is whether Hormuz physically reopens in the near term. The second is whether the underlying political situation in Iran resolves to a stable equilibrium that removes the energy risk premium structurally. Those are very different questions with very different answers.

When analysts model a geopolitical situation like this as having a single most-likely resolution, they are usually making an error. Iran’s political system is currently under severe stress across multiple dimensions simultaneously—military capacity, economic function, institutional legitimacy, and leadership succession. Systems under this kind of compound stress do not resolve predictably. They produce a wide distribution of outcomes.

First, the IRGC and its affiliates are not the only actors to consider. Iran is a far more ethnically and regionally complex country than its projected image of theocratic uniformity suggests. Khuzestan—the Arab-populated province that sits atop the majority of Iran’s oil infrastructure—has a long history of separatist grievance and was the primary battleground of the Iran–Iraq war. Iranian Kurdistan has cross-border connections to Kurdish movements in Iraq and Syria. Baluchistan, Sunni and historically marginalized, has sustained an active insurgency for years. The Turkic Azerbaijani population in the northwest sits next to an emboldened Azerbaijan that has recently demonstrated its willingness to act on territorial ambitions. Arab tribes along the Gulf littoral have their own relationships to these waters that predate the Islamic Republic entirely.

In a stable, functioning Iranian state, these fault lines are managed—sometimes brutally—by a security apparatus with the capacity to project force across the country. In an imploding state, that calculus changes entirely. These groups do not need a unified agenda or a coordinated command structure to cause significant disruption. They need only for the security apparatus to be sufficiently degraded that local action becomes viable. Some of them are located very close to exactly the infrastructure and waterways that matter most for global energy markets.

The realistic scenarios for Iran over the next 12 to 36 months span a significant range: managed degradation into a rump state; elite fracture leading to back-channel accommodation with the West; prolonged fragmentation with no central authority capable of negotiating anything; popular revolution and regime change; or a tactical ceasefire that freezes the conflict without resolving it.

The fragmentation scenario deserves particular attention because it is, in my view, the most systematically underpriced by markets and the one the consensus is least prepared for. It is also the scenario where Iran’s internal ethnic and regional complexity becomes most consequential. A fragmenting Iran is not simply a weakened Iran—it is a country in which multiple power centers, ethnic movements, and regional factions each retain sufficient local capacity to disrupt energy infrastructure and shipping on their own initiative, without coordination, and without any single authority capable of delivering or enforcing a ceasefire even if they wanted to. There is nobody to negotiate with because there is nobody who speaks for the system as a whole. This is not a hypothetical—it is a description of what post-Gaddafi Libya has looked like for 15 years.

Each scenario carries different energy implications. Regime change in a pragmatist direction could eventually be disinflationary for oil, as a normalizing Iran would seek to monetize its reserves. Fragmentation produces sustained, structurally intractable disruption for precisely the reasons described above. A frozen conflict is a staging post toward one of the other outcomes, not a destination in itself. The probability-weighted energy impact of this full distribution is materially higher than what crude curves are currently pricing.

People who have not spent time in the Gulf tend to think of Hormuz as a shipping lane that can be opened or closed by political decision—that a ceasefire announcement is roughly equivalent to a reopening. It is not that simple, and the geography is the reason.

The Strait of Hormuz is approximately 21 miles wide at its narrowest point, but the navigable shipping channels—the lanes deep enough and wide enough for laden supertankers—are only about two miles wide in each direction, separated by a two-mile buffer zone. This is not open water. It is a defined, constrained corridor, and every vessel transiting it knows exactly where it has to be.

That geometry matters enormously for risk assessment. A ceasefire between governments does not demobilize every IRGC splinter faction or other militia groups that may arise. These groups do not necessarily take orders from whoever is conducting back-channel negotiations in a hotel in Oman. A single mine in a two-mile channel—placed by an actor with no interest in the diplomatic process—can close that channel to commercial traffic for weeks while it is swept. A single successful strike on a vessel in that corridor triggers an insurance withdrawal that shuts traffic far more effectively than any blockade.

The insurance market understands the cumulative weight of these risks even if the diplomatic headlines do not. When the insurance market and the diplomatic market are giving you different signals, I have learned—from experience—to pay more attention to the insurance market.

The distinction between crude oil tankers and LNG carriers is not well understood outside the industry, and it matters significantly for the energy price argument.

A very large crude carrier—a VLCC—taking a hit in the Strait of Hormuz is a catastrophic event for its crew, its owner, and its insurer. It is a contained catastrophe in the sense that the vessel burns, sinks, or is disabled, and the channel eventually reopens.

A laden LNG carrier taking a hit in the same location is a different category of event entirely. These vessels carry liquefied natural gas at temperatures of around minus 162 degrees Celsius. They are, in the bluntest terms, extremely large and extremely sophisticated floating energy storage systems. A successful strike does not simply sink the vessel—it creates a hazard whose consequences for the surrounding waterway, for other shipping, and potentially for the physical infrastructure of the channel itself are of a fundamentally different order.

LNG carrier operators and their insurers understand this perfectly well. LNG carriers will be the last category of vessel to return to Hormuz transit following any ceasefire, and they will require a substantially higher threshold of demonstrated security before doing so—one that a fragmented threat environment, with multiple independent actors and no single authority capable of enforcing a ceasefire on all of them, may be very slow to provide.

Additionally, Ras Laffan—the world’s largest LNG facility, handling a significant proportion of global LNG supply—has already suffered infrastructure damage. Restart timelines are measured in weeks to months. And even when the facility is operational, getting the cargoes out through a waterway that LNG operators do not yet trust is a separate problem entirely.

The spot price moves in LNG are significant. But the more consequential story for long-term investors is what happens to the structure of global LNG supply agreements from this point forward—and this story will unfold over years, not weeks.

Asian and European utilities are right now sitting across the table from their boards, their regulators, and in some cases their governments, with a very visible, very quantifiable insurance premium on Gulf-sourced supply that did not exist 18 months ago. European natural gas storage entered this crisis critically depleted—roughly 46 billion cubic metres (bcm) at the end of February 2026, against 60 bcm a year earlier. The legal mandate to refill to 90% by November creates inflexible, non-deferrable demand through the summer regardless of price.

The 2022 Russian gas episode established the template for what happens next: Europe did not meaningfully return to Russian gas when the conflict paused. It rewired its supply chain, permanently. Counterparty risk, once made legible at sovereign scale, does not become illegible again simply because the shooting stops. The risk has been made visible. It cannot be made invisible again.

The main beneficiaries—but not only—of this structural shift are Australian and North American LNG producers, who will systematically receive a contracting premium over Qatari supply in the new agreement cycle—not because Qatar is permanently offline, but because the diversification premium is now politically and commercially non-negotiable for buyers. A ceasefire headline may look like the thesis ending. It is more likely that the thesis is beginning its slower, more durable phase.

Four practical implications for advisor thinking:

Disclosure: This material is for informational purposes only and should not be considered investment advice. An investor should consult with their financial professional before making any investment decisions. The opinions contained herein are subject to change without notice and do not necessarily reflect the opinions of Rayliant Investment Research. Indices cannot be invested in directly and are unmanaged.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED