“The United States — we produce more oil than we can consume. We’re a net oil exporter.”

—Chris Wright, US Energy Secretary, interviewed by Fox News on March 12, 2026

When the Bureau of Labor Statistics released US inflation statistics for March a couple weeks back, the CPI showed a 0.9% month-over-month increase: a reading hotter than the 0.3% rise in February and one that puts US prices 3.3% higher year-over-year. Driving the action, unsurprisingly, was a 10.9% monthly rise in energy prices, including a 21.2% March increase in the price of gasoline. In light of claims that US “energy dominance” would insulate America’s economy from a shock to Gulf oil prices—exemplified in US Energy Secretary Chris Wright’s quote above—it’s worth unpacking how disruptions to other countries’ oil supply feed back to prices US households pay at the pump.

One of the first potential misconceptions is that there’s a single definition of “energy”—or even “oil”—that America might export and import or produce and consume. When politicians and pundits talk about America’s “net exporter” status, they’re likely referring to a broad category of “crude oil and petroleum products,” and the US did become a net exporter, on that definition, back in 2020. But if we restrict to just the “crude oil” bit, suddenly the US flips to a net importer, bringing in over 6 million barrels per day and shipping out just under 4 million. So, even though the US sits atop the rankings as the greatest producer of crude oil, it still buys plenty from other producers, including those stuck behind an inconvenient blockage of the Strait of Hormuz.

Of course, this distinction raises another question: If the US needs more of the oil it’s drilling, why not just hold onto those barrels as opposed to shipping them abroad? The answer to that question goes back, in large part, to the time before America became such a powerhouse of production. In those days, the US was importing loads of Middle East oil, which happens to be heavy and “sour”—a concise way of saying it has higher sulfur content—versus the less viscous and more highly prized “light sweet” crude characteristic of most US production. As such, most US refineries are built to process foreign oil, not the oil American wells are producing, necessitating all of that import–export action we see in statistics covering trade in these different grades of crude.

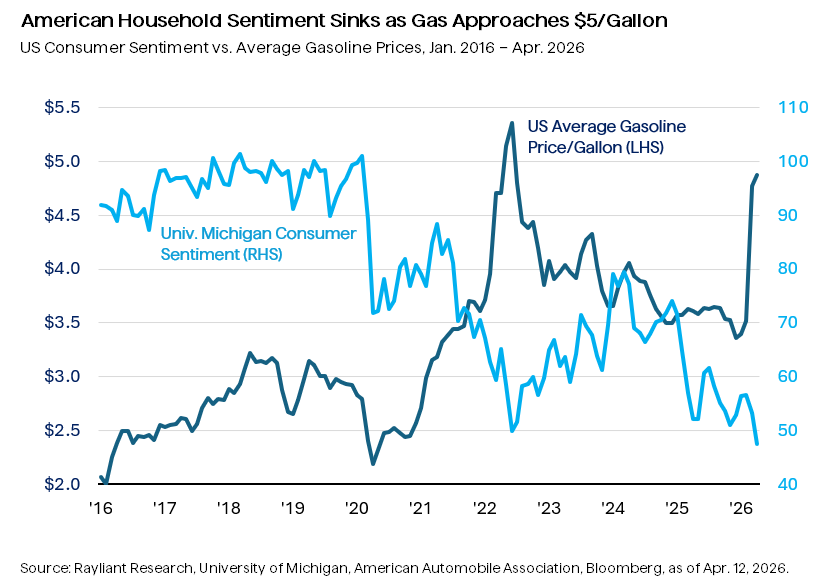

Finally, even if America did incur the massive costs required to overhaul its refineries for processing domestic oil into gasoline, there are two further challenges really capitalizing on the idea of “energy dominance.” For one thing, while US oil and gas companies do produce more crude oil than any other nation on earth, US businesses and households also consume more oil than anyone else on the planet. For another, regardless of where oil is produced or who’s buying and selling it, the price of that oil is set in the global market, and that is impacted by shocks like the one experienced by Gulf oil suppliers in March. That’s why, when shipping through the Strait of Hormuz ground to a halt a month ago, prices at gas pumps a world away in the US rocketed up, as seen below.

According to reporting by Axios, the 2026 Iran War represents, by at least one measure, the greatest global oil supply disruption on record, with 16% of global supply taken off the market, comparing to losses of just 8% share in the case of both Iraq’s invasion of Kuwait back in 1990 and the 1973 oil embargo. Many experts believe we’re only beginning to see the impact of that hit to prices and that the effects could be with us for quite some time. The implications of a prolonged shock to energy costs could be severe, affecting not just inflation, but also US consumer confidence. In the chart above, we’ve plotted household sentiment tracked by the University of Michigan, which fell in April to the lowest point in the survey’s 74-year history, mirroring the rise in gas prices. Given consumer spending makes up roughly two-thirds of US GDP, and with midterm elections just months away, observers on Wall Street and Pennsylvania Avenue will no doubt be hoping a quick end to Middle East conflict might soon bring prices and sentiment back to a happier place.

Disclosure: This material is for informational purposes only and represents the views of Rayliant Investment Research as of the date of publication, which are subject to change without notice. This material should not be considered investment advice or a recommendation to buy or sell any security or asset class. Statistical data and other information contained herein have been obtained from sources believed to be reliable; however, Rayliant does not warrant the accuracy or completeness of such information. An investor should consult with their financial professional before making any investment decisions.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED