“Interest rates are to asset prices like gravity is to the apple.

They power everything in the economic universe.”

—Warren Buffett

Given investors’ anxiety over technology stocks so far this year—amidst what some have referred to as the “AI scare trade”—it would be easy to conclude that 2025’s strong sentiment toward the US economy and stock market had given way to a more pessimistic mindset. In one area, though, investors seem to be feeling much better vibes: the outlook for Fed rate cuts in 2026.

In part, that’s because of a growing recognition that in a few short months, President Trump will finally get his wish for a new Fed chair, as current head Jerome Powell’s tenure ends and the president’s pick, Kevin Warsh, most likely takes the helm. But it’s also down to fundamentals. After suffering lingering effects of a virtual macro information blackout at the hands of last year’s lengthy government shutdown, we’re also finally starting to get some good data on America’s economy.

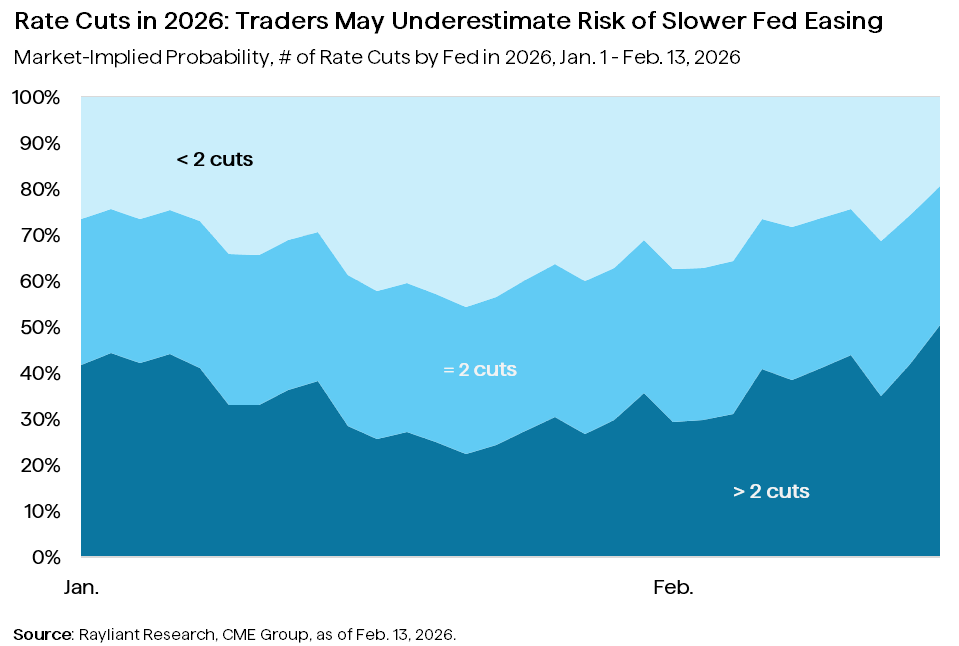

Those numbers are telling us where matters stand on the Fed’s dual mandate—holding inflation at bay while supporting robust employment—and have also been driving some strong action in derivatives priced according to traders’ beliefs of when and by how much the US central bank is likely to cut rates. Below, we’ve plotted those futures’ price changes since 2026 began.

Mid-February turned out to mark an important milestone for those hoping to see more easing this year, as the probability of three or more rate cuts in 2026—a number that had wavered substantially since the beginning January—finally crossed 50% and became the more-likely-than-not outcome. Strong January jobs data released on February 11, 2026, didn’t help the doves’ case, but a softer-than-expected January CPI released just two days later gave investors hope that a more Trump-friendly Fed might see its way to a third cut, with easing seen resuming by June or July.

Watching unconditional AI enthusiasm fading, previously high-flying hard assets like gold, silver, and cryptos crumbling, and a slew of geopolitical risks brewing perilously in the background—all worries we’ve weighed in past commentary—it seems that policy rate reductions couldn’t come at a better time to keep the rally in risk assets going. Before jumping to conclusions on the magnitude and timeline for future rate cuts, we believe it’s worth considering factors that could influence the odds on the other side of that coin.

Let’s start with the new Fed chair arriving in May, and let’s set aside the fact that Mr. Warsh is seen as one of the more hawkish candidates Trump might have tipped for the job. He’s still but one of 12 voting members of the FOMC, only two of whom—Governors Miran and Waller—appear decisively dovish. Indeed, we’ve watched dissent among the committee’s members rising as the Fed funds rate has fallen, and it wouldn’t surprise us in the least if the group retains its independent spirit in spite of White House hopes for a more accommodative central bank, post-Powell.

Delving deeper into the data, it’s also easy to see where cracks in the fundamental case for faster cuts might emerge. We’ve already referenced strong jobs numbers raising the bar for further easing. On the inflation side of things, we note that January’s favorable headline number hinged mostly on falling energy costs: a trend that could turn as oil prices rise. Moreover, anecdotal evidence from the Fed’s own Beige Book suggests companies’ willingness to absorb the tariff shock and protect consumers from rising prices might finally have reached its limit, which could see progress on inflation stall just a little too far above the Fed’s 2% target.

So, though it’s easy to imagine a pair of rate cuts coming in the second half of this year—and that’s the degree of easing predicted by the Fed’s last dot plot, and our current base case—we also have doubts. In light of the risks we’ve just described, we worry traders may, in jumping out to a forecast of three or more quarter-point reductions by December, be putting too much weight on the possibility of a positive surprise and could be overlooking the possibility “higher for longer” policy makes an unwelcome return in 2026.

Disclosure: This material is for informational purposes only and should not be considered investment advice. An investor should consult with their financial professional before making any investment decisions. The opinions contained herein are subject to change without notice and do not necessarily reflect the opinions of Rayliant Investment Research. Indices cannot be invested in directly and are unmanaged.

You are now leaving Rayliant.com

The following link may contain information concerning investments, products or other information.

PROCEED